Westside Story Newspaper – Online The News of The Empire – Sharing the Quest for Excellence

Westside Story Newspaper – Online The News of The Empire – Sharing the Quest for Excellence

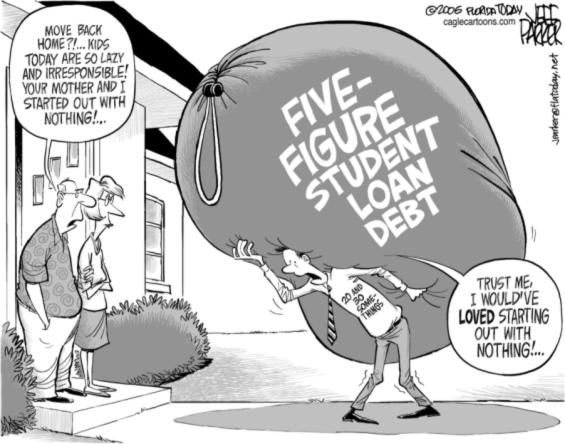

July 1 is an important date for students and families: it’s when most changes to federal student aid – both loans and grants – go into effect. For the year starting July 1, 2016, new federal loans for undergraduates, graduate students, and parents will have lower fixed interest rates than loans taken out the year before, and the maximum Pell Grant will be higher. To help inform college borrowing decisions, there is a new easy-to-read chart with 2016-17 interest rates, loan amounts, and other useful information for the most common types of federal loans.

July 1 is an important date for students and families: it’s when most changes to federal student aid – both loans and grants – go into effect. For the year starting July 1, 2016, new federal loans for undergraduates, graduate students, and parents will have lower fixed interest rates than loans taken out the year before, and the maximum Pell Grant will be higher. To help inform college borrowing decisions, there is a new easy-to-read chart with 2016-17 interest rates, loan amounts, and other useful information for the most common types of federal loans.

The coming changes include:

- On July 1, the maximum Pell Grant will be adjusted for inflation to $5,815, up from $5,775. Pell Grants help nearly eight million lower income students pay for college and limit how much they need to borrow.

- The new maximum grant for will cover less than 30% of the cost of attending a public four-year college, the smallest share in over 40 years. And under current law, the maximum Pell Grant will no longer be tied to inflation after 2017-18.

- On July 1, the fixed rates for new federal loans will be lower than the rates for loans issued last year.

- Stafford loans for undergraduates, subsidized and unsubsidized: 3.76% for loans issued in 2016-17 (down from 4.29% for loans issued in 2015-16).

- Stafford loans for graduate students: 5.31% for loans issued in 2016-17 (down from 5.84% for loans issued in 2015-16).

- Parent and Graduate PLUS loans: 6.31% for loans issued in 2016-17 (down from 6.84% for loans issued in 2015-16).

- On October 1, origination fees will increase slightly for new federal loans.

- For loans issued October 1, 2016 through September 30, 2017, fees will be 1.069% of principal for all Stafford loans (up from 1.068%), and 4.276% for all PLUS loans (up from 4.272%).

For more information about federal student loans for the coming school year, see the summary chart, Federal Student Loan Terms for 2016-17 below:

This chart summarizes the interest rates, loan limits, and other terms for federal student loans issued from July 1, 2016 through June 30, 2017.

Basic Eligibility Requirements

| U.S. citizens or permanent residents, enrolled at least half time in a qualified program at a participating school, not in default on a prior federal student loan, and not previously convicted of a drug offense while receiving federal financial aid. Total aid, including student loans, cannot exceed the school’s total cost of attendance (tuition and fees, room and board, transportation, personal and miscellaneous expenses). FAFSA required. |

Stafford Loans

| TYPES | Subsidized Stafford Loan: Available only to undergraduate students on the basis of financial need. No credit check required. The federal government covers the interest on these loans while borrowers are enrolled at least half time and for six months after they are no longer enrolled at least half time. Monthly payments are not required until six months after leaving school. |

| Unsubsidized Stafford Loan: Available to undergraduate and graduate students regardless of financial need. No credit check required. Interest is charged throughout the life of the loan. Monthly payments are not required until six months after leaving school. | |

| ANNUAL LOAN LIMITS | Dependent undergraduates (most students under the age of 24): $5,500 as freshmen (including up to $3,500 subsidized); $6,500 as sophomores (including up to $4,500 subsidized); $7,500 as juniors and seniors (including up to $5,500 subsidized). |

| Independent undergraduates (students age 24 or older) and dependent students whose parents are unable to obtain PLUS Loans: $9,500 as freshmen (including up to $3,500 subsidized); $10,500 as sophomores (including up to $4,500 subsidized); $12,500 as juniors and seniors (including up to $5,500 subsidized). | |

| Graduate students: $20,500 (or $40,500 for certain medical training). | |

| AGGREGATE LOAN LIMITS | Dependent students: $31,000. Independent undergraduates and dependent students whose parents are unable to obtain PLUS Loans: $57,500. Graduate and professional students: $138,500 (or $224,000 for certain medical training) including undergraduate borrowing. |

| INTEREST RATES | The interest rate for undergraduate Stafford loans, both subsidized and unsubsidized, is 3.76%. Rates are fixed for the life of the loan. (See how interest rates are determined.) |

| The interest rate for unsubsidized Stafford loans made to graduate students is 5.31%. Rates are fixed for the life of the loan. (See how interest rates are determined.) | |

| FEE | 1.068% if first disbursed on or after October 1, 2015 and before October 1, 2016; 1.069% if first disbursed on or after October 1, 2016 and before October 1, 2017. |

| ELIGIBILITY PERIOD FOR SUBSIDIZED LOANS | New borrowers are only eligible to receive subsidized Stafford loans for a time period that is 150% of the published length of their program. After that, borrowers are not eligible to receive additional subsidized loans and may become responsible for interest that accrues on their existing loans. Borrowers with any federal loans from before July 1, 2013 are not affected. For more information on the maximum eligibility period, please see studentaid.gov. |

PLUS Loans

| TYPES | Parent PLUS: Loans to parents of dependent students to help pay for undergraduate education. Parents are responsible for all principal and interest. |

| Grad PLUS: Additional loans to graduate and professional degree students to help cover education expenses. | |

| ADDITIONAL ELIGIBILITY REQUIREMENTS | Available regardless of financial need to parents of dependent students (Parent PLUS) and to graduate and professional students (Grad PLUS). Credit check required. The credit requirement can be met by a cosigner. May require a separate application in addition to the FAFSA. |

| LOAN LIMIT | Total cost of attendance minus other financial aid. No aggregate maximum. |

| INTEREST RATE | 6.31% (See how interest rates are determined.) |

| FEE | 4.272% if first disbursed on or after October 1, 2015 and before October 1, 2016; 4.276% if first disbursed on or after October 1, 2016 and before October 1, 2017. |

How Interest Rates are Determined

| FIXED RATE LOANS | All Stafford and PLUS loans originated since July 1, 2006 have fixed rates. Since 2013, fixed rates for new loans are set each year based on the 10-year Treasury note following the May auction (1.710% for 2016-17) plus a set margin of 2.05 percentage points for undergraduate Stafford, 3.60 points for graduate Stafford, and 4.60 points for PLUS loans. Although rates for new loans are set each year, rates are fixed for the life of the loan. |

| VARIABLE-RATE LOANS | For older Stafford and PLUS loans with variable rates, interest rates change annually on July 1, based on the last 91-day T-bill auction in May. |

During Repayment

| RATE REDUCTION FOR AUTOMATIC ELECTRONIC PAYMENTS | Borrowers can receive a 0.25% interest rate reduction if they sign up for auto debit payments online. |

| DEFERMENTS FOR UNEMPLOYMENT OR ECONOMIC HARDSHIP | Borrowers may defer payments for up to three years. For Parent PLUS, Grad PLUS, and unsubsidized Stafford Loans, interest continues to accrue. For more about other repayment options, see studentaid.ed.gov. |

| INCOME-DRIVEN REPAYMENT PLANS | There are several income-driven repayment plans that can help keep payments manageable by capping them at a low percentage of the borrower’s income: Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income Contingent Repayment (ICR). Borrowers who make payments based on their income can receive a discharge of their remaining student debt after 20 or 25 years of payments For more information about these plans and to estimate monthly loan payments, see studentaid.ed.gov/idr and IBRinfo.org. |

| PUBLIC SERVICE AND TEACHER LOAN FORGIVENESS | Public Service Loan Forgiveness is available after 10 years of qualifying payments and employment, only for Direct Loans (excluding Parent PLUS, unless consolidated). The Teacher Loan Forgiveness Program (Stafford only) is available for loans in both the Direct and FFEL programs. All federal loans issued since July 1, 2010 are Direct Loans. Teachers with Perkins loans may be eligible for a loan cancellation if they meet certain requirements. More information for teachers can be found at studentaid.ed.gov. |

| LOAN CONSOLIDATION | Borrowers with Direct and/or FFEL loans can convert them into a Direct Consolidation loan. There is no fee. Depending on the borrower’s total debt, repayment periods can vary from 10 to 30 years. For more information, see studentaid.gov. To apply online, go to studentloans.gov. |